What to invest in 401K? This is a question that every employee who's employer provides this retirement savings plan must answer for "themselves" as this is probably the biggest of the financial vehicles we use to secure our financial future, if this is the only bucket in which you invest.

I have answered this question for myself, but not always by myself, from the choices that I have in my company's savings plan. It has 9 mutual fund choices and 12 target date retirement funds, but what is the best combination to have? At one point, I left that up to the expertise of a financial advisor which put together a portfolio for me based upon my financial profile. Once they have this then poof, out comes your asset allocation and off you go. I don't even think I ever talked to an advisor. I just received a quarterly statement of my portfolio's performance and I would check it to see if it was going up.

However, I wanted to know more about my 401K, what to invest in 401K, was it even a good idea to invest in 401K? So I went to library and read books on the topic to get general understanding on what to do and I really did learn something and continue to learn mostly that I "can" make these investment decisions by myself if I educate myself first. I mean I know for me, I could confidently choose which investments I want to be in my 401K from the options my company plan provided. Based upon what I know now, it came down to finding the one(s) that charged the least amount of fees. By finding that alone, you have eliminated the actively managed funds and one of the potential drags on your returns. Don't get me wrong, I wanted good performance as well, but in reading Jack Bogle's research on the markets and the history of asset managers who run these mutual funds to under-perform their benchmarks after fees, it became clear what to invest in 401K.

So, I went through my company's prospectus for the funds I had to chose from and found the one(s) with the lowest fees which happed to a S&P 500 Index Fund (S&P 500 which only had annual charge of $.90 per $1,000) and my company's fund. Then I called, who at the time, was my financial advisor to change my asset allocation (an assortment of different Target Date Retirement Funds) to be 98% S&P 500 Index Fund and 12% my company's stock. They told me that they would not be able to allocate more than 9% in my company's stock and still manage the portfolio. Well, this was the crossroad where I could take the wheel because I knew I had educated myself and I knew what I wanted in my portfolio and they couldn't give it to me how I wanted it. So, I said alright I'll manage it myself.

That is exactly what I did, and a bit of luck was involved because this was right before the run up in the stock market after 2009 crash; however, I knew too that the S&P covers a large swath of stocks in the market and it is the benchmark most asset fund managers performance are measured by. I also knew I wanted a more equity laden portfolio given the state of bonds now and I couldn't achieve that simply with the Target Date Retirement Funds. However, that for me would have been my other choice had the S&P 500 Index Fund not been available.

It was good to learn that I could find the cheapest of my selection of funds and still do very well. I will pretty much get what the market gives me good or bad using this strategy because the S&P 500 Index Fund is not actively managed, it just tracks the S&P 500. It gave me confidence too, that though I, a meager not supposed to understand this stuff, took ownership in the management of my retirement fund, I didn't fail.

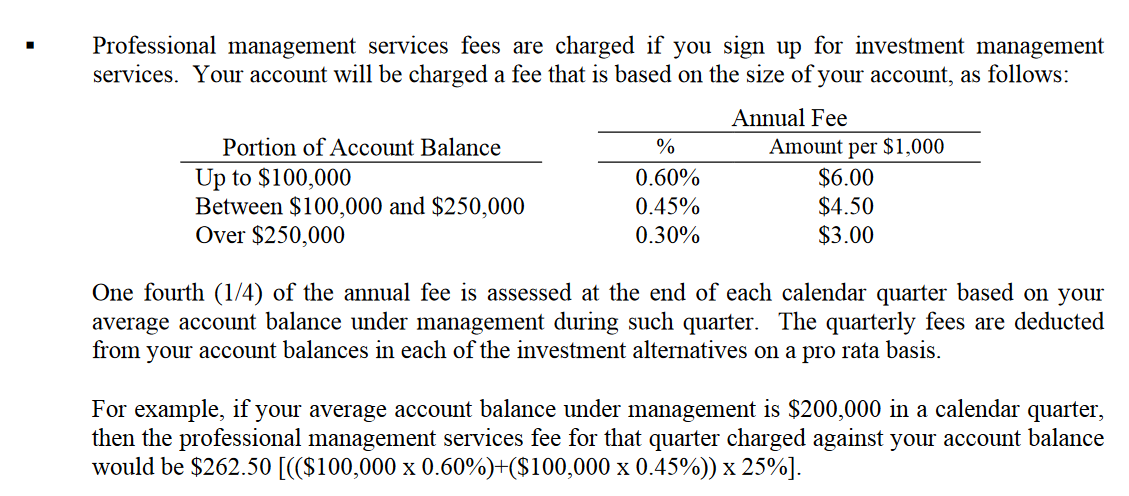

By knowing what to select to invest in, I also eliminated another middle man to my money, that being my financial advisor. I am not trying to belittle the financial advisor, but I am a little, because some people need their guidance, I did at one time as well! However, unbeknownst to me, not that they charged a fee, but how much it was costing me in lost opportunity cost (the loss of potential gain from other alternatives when one alternative is chosen). See the below on how the advisors charge on an account and then extrapolate that out over years of investing.

In addition, if you didn't know a small fact, they get paid much like asset managers do regardless if your portfolio is up or down. So just imagine if you will, it is 2009 all over again and you had $200,000 in your 401K and you lost $100,000 or 50% of it and your average for the quarter was now just over $150,000, using the above formula, you'd be charged $206 per quarter ($825 per annum). Talking about adding insult to injury, you have paper loss of $100,000 and your financial advisor says to you, and you owe me $825 ([(($100,000 x 0.60%)+($50,000 x 0.45%))]). WTF!? I didn't even mention the fees of the mutual funds if you happen to be invested in them as well. I give my advisors credit on one thing, they only had my portfolio in the lower fee Target Date Retirement funds and not the mutual funds.

After seeing this, wouldn't you rather that money compounding and growing for your future retirement, especially if you have another setback like 2009? I know I now do, especially with the cost of things ever increasing.

What the current state of my 401K portfolio is 50% S&P 500 Index Fund and 50% sort of cash until maybe the end of first quarter 2017. I have money in Stable Fund which is really disappointing because I really just wanted to have a portion of my funds in cash to be able to buy the dips in the market, but their isn't an option for that. They make it whereas you have to invest in something that has a fee associated to it and now I have to pay for that.

Note: Doing this post, I actually realized, I could have less fees if I invest in Target Date Income Fund as it's more income based. I will change tomorrow as the aforementioned Stable Fund has 0.49% or $4.90 per $1,000 as of December 31, 2015; whereas, the Target Date Income Fund has .17% or $1.70 per $1,000 as of December 31, 2015.

Nonetheless, I make due trying to set aside for the future and I only put into my 401K what my employer matches, anything else I want to invest, I do outside of my 401K where I have much more flexibility and control. I have gone back in forth with my decision to invest anything in my company's 401K plan given the lack of good options and lack of control you have to protect or capitalize on my investment when there are big shifts in the market. However, it is hard to pass up dollar for dollar match and letting the market do the rest to compound and hopefully grow your money over time. So, I'm in it for now and I know what to invest in 401K.

So, if you made it here the lesson of this blog is as follows:

- Educate yourself on investing in the stock market particularly with your 401K and know you too change manage your own financial assets

- Find the lowest fee fund(s) in your company's offering and invest in those or a simple Target Date Retirement Fund (which reallocates by itself it weighting in stocks and bonds based upon your age and other factors) in year you plan to retire

- Try to bypass mutual funds that are actively managed

- Try to keep some cash in your 401K to buy the dips in the market

- Think about firing your financial advisor, but only after you have properly educated yourself, hopefully sooner rather than later

PS: Please share your experience by leaving a comment on this post. Also please be sure share this content to your friends and family if you find it useful. I thank you in advance.

No comments:

Post a Comment